Are Reits out of the woods yet?

There are still clouds over the real estate investment trust (Reit) sec- tor following a spate of earnings results for the period ending June 30. Maybank analyst Krishna Guha said there are challenges from having to reprice debt at higher interest rates, while occupancy is up at some properties but not as strong at others.

At least rent reversions- the level at which new leases are signed or renewed - are still positive.

Meanwhile, the global economy remains challenging, especially given the hawkish tone taken by Unit- ed States Federal Reserve chairman Jerome Powell at the recent Jackson Hole conference. "Although inflation has moved down from its peak - a welcome development - it remains too high," he said.

So while markets were hoping that rate hikes would be eased, the door has now been left open to the possibility of further increases.

Phillip Securities Research senior research analyst Darren Chan said the Fed intends to keep rates at a restrictive level until it is sure inflation is significantly trending towards the 2 per cent goal. This stance also signifies the Fed's wilingness to hike rates further.

INTEREST RATES

The overriding factor for Reits is the fluid interest rate environment. This means the outlook for costs (including hedging) remains uncertain, said Mr Guha.

In general, rising interest rates pose more challenges for Reits than for stocks as Reits tend to have low- er growth and higher gearing. Higher rates tend to depress the

valuation of the properties unless offset by growth in operating income. They also mean increased borrowing costs. As Reits usually take on debt to acquire properties, the higher repayments will eat into distributions.

Reits are a popular investment for folk keen on a regular income stream, but they become less popular when rates rise as people can get the same yield elsewhere.

SingCapital chief executive Alfred Chia said: "Typically, Reits are sensitive to interest rate movements. As rates rise and stay high, it will affect the distribution per unit and reduce the yield to investors."

Still, Reits with strong fundamentals, including well-located proper- ties and stable cash flow, are more resilient to rising rates. Investors would need to do more research to find the suitable ones, he added.

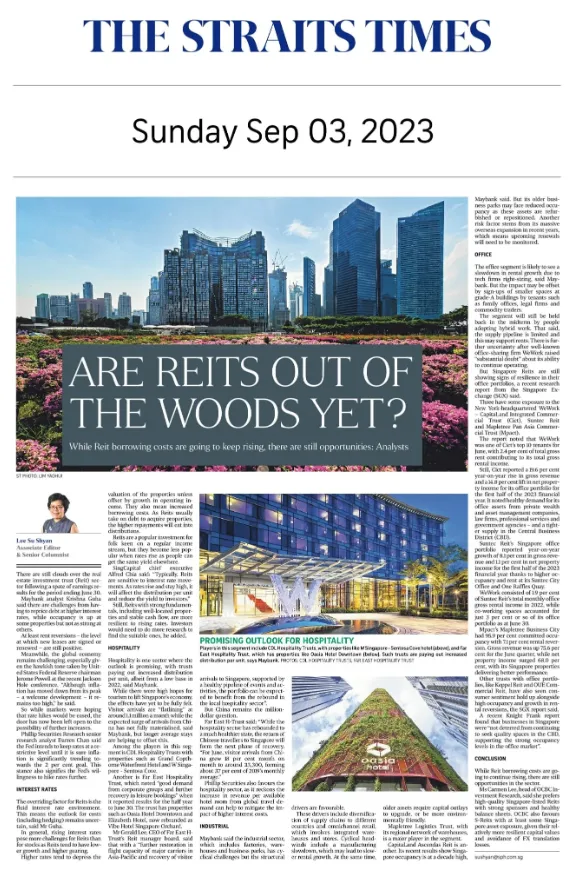

HOSPITALITY

Hospitality is one sector where the outlook is promising, with trusts paying out increased distribution per unit, albeit from a low base in 2022, said Maybank.

While there were high hopes for tourism to lift Singapore's economy, the effects have yet to be fully felt. Visitor arrivals are "flatlining" at around 1.1 million a month while the expected surge of arrivals from China has not fully materialised, said Maybank, but longer average stays are helping to offset this.

Among the players in this segment is CDL Hospitality Trusts with properties such as Grand Copthorne Waterfront Hotel and W Singa- pore Sentosa Cove.

Another is Far East Hospitality Trust, which noted "good demand from corporate groups and further recovery in leisure bookings" when it reported results for the half year to June 30. The trust has properties such as Oasia Hotel Downtown and Elizabeth Hotel, now rebranded as Vibe Hotel Singapore Orchard.

Mr Gerald Lee, CEO of Far East H- Trust's Reit manager board, said that with a "further restoration in flight capacity of major carriers in Asia-Pacific and recovery of visitor

arrivals to Singapore, supported by a healthy pipeline of events and activities, the portfolio can be expect- ed to benefit from the rebound in the local hospitality sector".

But China remains the million- dollar question.

Far East H-Trust said: "While the hospitality sector has rebounded to a much healthier state, the return of Chinese travellers to Singapore will form the next phase of recovery. "For June, visitor arrivals from China grew 18 per cent month on month to around 113,300, forming about 37 per cent of 2019's monthly average."

Phillip Securities also favours the hospitality sector, as it reckons the increase in revenue per available hotel room from global travel demand can help to mitigate the im- pact of higher interest costs.

INDUSTRIAL

Maybank said the industrial sector, which includes factories, ware- houses and business parks, has cyclical challenges but the structural

oasia hotel

drivers are favourable. These drivers include diversification of supply chains to different countries and omnichannel retail, which involves integrated warehouses and stores. Cyclical head- winds include a manufacturing slowdown, which may lead to slow- er rental growth. At the same time,

older assets require capital outlays to upgrade, or be more environmentally friendly.

Maybank said. But its older business parks may face reduced occupancy as these assets are refurbished or repositioned. Another risk factor stems from its massive overseas expansion in recent years, which means upcoming renewals will need to be monitored.

OFFICE

The office segment is likely to see a slowdown in rental growth due to tech firms right-sizing, said May- bank. But the impact may be offset by sign-ups of smaller spaces at grade-A buildings by tenants such as family offices, legal firms and commodity traders.

The segment will still be held back in the midterm by people adopting hybrid work. That said, the supply pipeline is limited and this may support rents. There is further uncertainty after well-known office-sharing firm WeWork raised "substantial doubt" about its ability to continue operating.

But Singapore Reits are still showing signs of resilience in their office portfolios, a recent research report from the Singapore Ex- change (SGX) said.

Three have some exposure to the New York-headquartered WeWork - CapitaLand Integrated Commer- cial Trust (Cict), Suntec Reit and Mapletree Pan Asia Commercial Trust (Mpact).

The report noted that WeWork was one of Cict's top 10 tenants for June, with 2.4 per cent of total gross rent contributing to its total gross rental income.

Still, Cict reported a 19.6 per cent year-on-year rise in gross revenue and a 14.8 per cent lift in net proper- ty income for its office portfolio for the first half of the 2023 financial year. It noted healthy demand for its office assets from private wealth and asset management companies, law firms, professional services and government agencies - and a tight- er supply in the Central Business District (CBD).

Suntec Reit's Singapore office portfolio reported year-on-year growth of 8.1 per cent in gross revenue and 1.1 per cent in net property income for the first half of the 2023 financial year thanks to higher occupancy and rent at its Suntec City Office and One Raffles Quay.

WeWork consisted of 1.9 per cent of Suntec Reit's total monthly office gross rental income in 2022, while co-working spaces accounted for just 3 per cent or so of its office. portfolio as at June 30.

Mpact's Mapletree Business City had 95.9 per cent committed occupancy with 7.1 per cent rental reversion. Gross revenue was up 75.6 per cent for the June quarter, while net property income surged 68.0 per cent, with its Singapore properties delivering better performance.

Other trusts with office portfolios, like Keppel Reit and OUE Commercial Reit, have also seen consumer sentiment hold up alongside high occupancy and growth in rental reversions, the SGX report said. A recent Knight Frank report found that businesses in Singapore were "not deterred from continuing to seek quality spaces in the CBD, supporting the strong occupancy levels in the office market".

SingCapital

Copyright © SingCapital Pte Ltd 2026. All rights reserved. This website or publication has not been reviewed by the Monetary Authority of Singapore (MAS).

Contact Us

+65 68014088

1 Kim Seng Promenade Great World City, Office East, Tower 12-06, 237994

Follow Us

A member of